As efforts to bail out fossil fuel polluters begin in earnest, millions of Americans are struggling with unprecedented job loss and a real economy that remains nearly frozen.

That gulf, between companies tapping billion-dollar safety nets and families barely getting by, raises a crucial question of equity: Are the Federal Reserve and Treasury handling taxpayer dollars as carefully as Americans who must slash their budgets to weather the pandemic?

A review of fossil fuel industry credit ratings suggests some cause for concern.

Credit ratings describe how likely an investor in a given bond or company is likely to be repaid. Independent agencies like S&P and Moody’s assign them to companies and to specific bonds issued by those companies.

A company’s credit ratings determine whether it can tap the Fed’s bailout programs. The goal is to support companies that were strong before COVID-19, so they can weather the economic storm and eventually stand on their own.

Ratings across the fossil fuel industry reflect widespread weakness that should disqualify them from these programs. An alarming number of fossil fuel companies just barely meet the Fed’s standard which has been weakened and is already lower than the one used by more conservative investment managers.

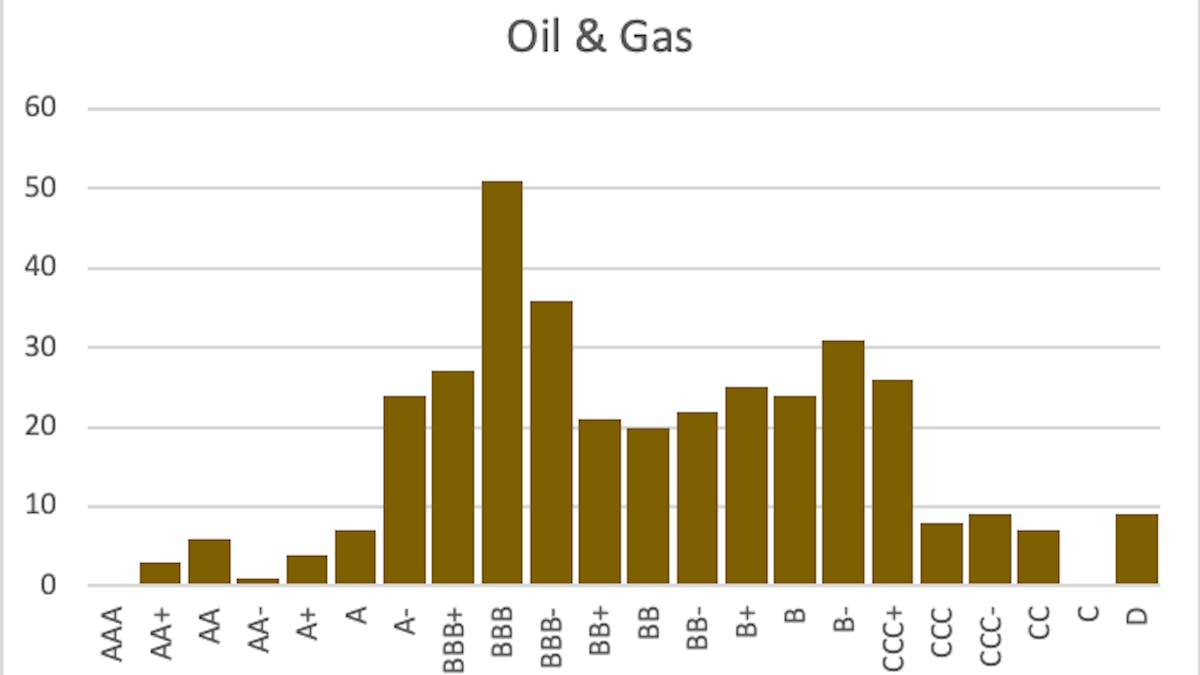

For example, less than half of the companies in the oil and gas sector carry the Fed’s minimum credit rating of BBB-, according to data from S&P Global Markets. Of these, nearly half fall just on the line, or one small notch above it. The Fed may help companies that carried that rating on March 22, even if they were downgraded since then.

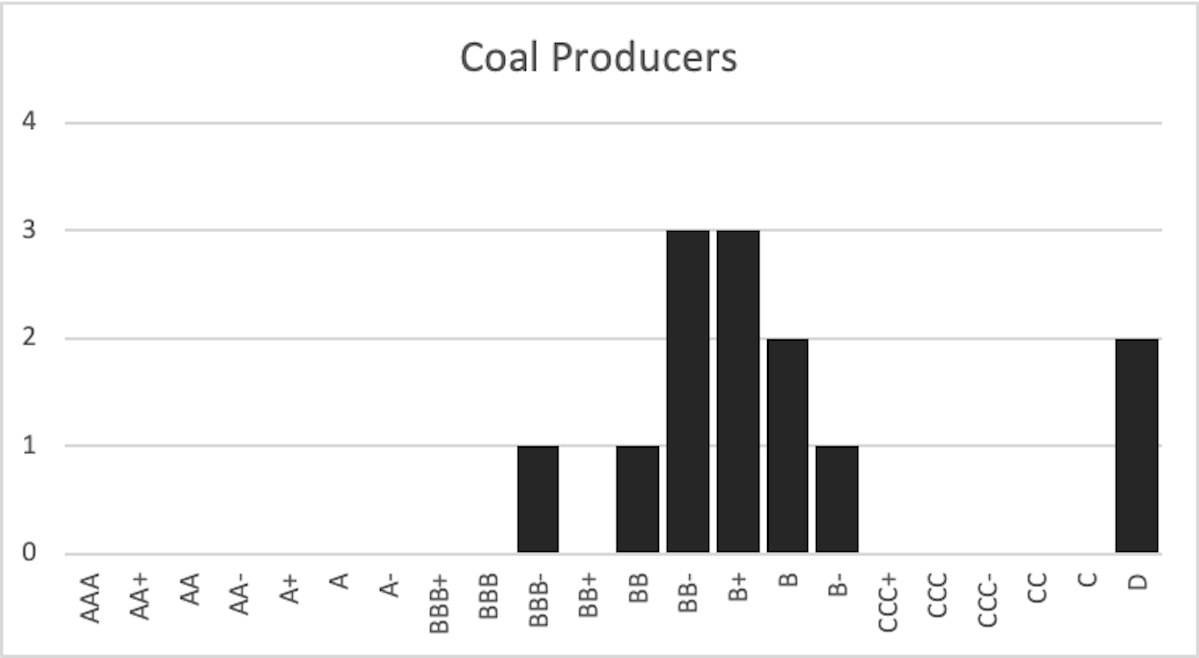

For coal, things are even gloomier. Only one company, representing 7% of the sector, meets the Fed’s standards. Coal-heavy utilities fare better, but even in this sector some companies fall below the Fed’s investment standards.

Across coal, oil, and gas, most companies saw their credit ratings downgraded long before the pandemic.

Although stronger than their peers, companies that meet Fed’s standards operate in the same industries and face the same existential threats, including massive debt burdens and long-term trends away from carbon-emitting energy production.

That means they’re not immune from the wave of bankruptcies roiling the industry in recent years. When some of them fail, they risk taking taxpayer funds with them.

Despite the industry’s ongoing crisis, fossil fuel companies have lobbied aggressively for even more access to Fed bailout funds. They want the Fed to buy bonds that are too risky for the average person’s 401k.

The Fed’s bond-buying is financed by money under the massive CARES Act stimulus package. The Treasury provided the Fed with taxpayer money to absorb future losses on its investments.

Given the fiscal challenges facing taxpayers, state governments, and industries that can contribute to a sustainable recovery, it’s growing hard to justify bailouts for an industry that the market has already started phasing out.