Fossil fuel companies solidified their dominant position as top beneficiaries of the Federal Reserve’s Main Street Lending Program in November, collecting more outsized loans of tens of millions of dollars than any other sector, even as clean energy companies’ small share of the program's benefits dwindled.

The results, based on a BailoutWatch analysis of Fed data released last week, highlight a dilemma facing the incoming administration, which must decide whether to redesign the programs to support a sustainable recovery after President-elect Joe Biden takes office in January. The data also vindicate successful lobbying earlier this year by oil and gas interests to reshape the program, ensuring it would lend to fossil fuel companies whose heavy debt burdens and structural problems could have ruled them out.

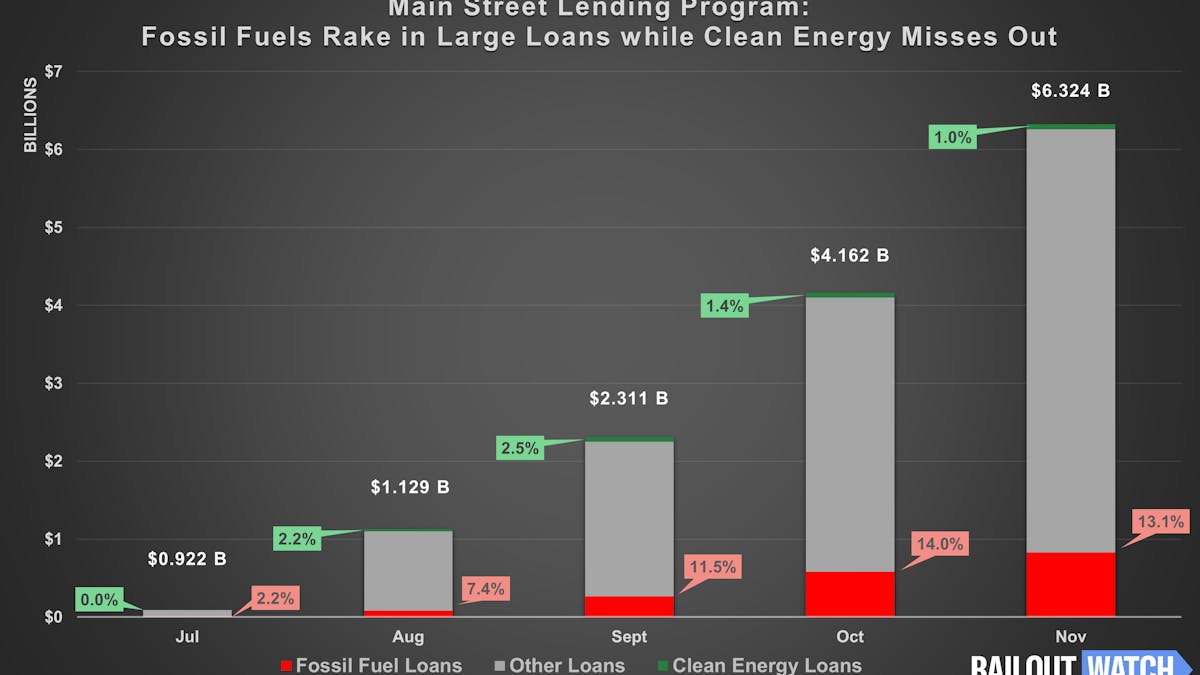

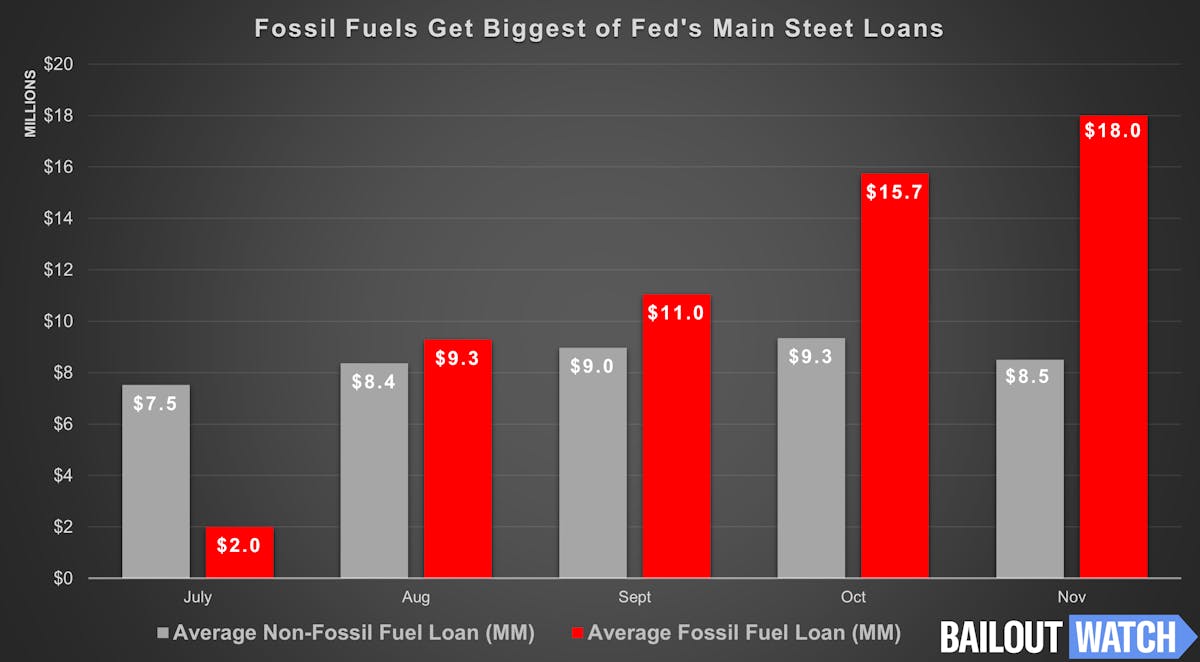

Forty-six fossil fuel companies have received Fed-subsidized loans totaling $828 million since the program started in July. The average loan size, $18 million, is nearly double the program’s average loan size of $9.8 million, or $9.2 million excluding fossil fuels. Twelve of the fossil fuel loans were worth $35 million or more, accounting for more than 30% of the program’s loans of that magnitude. See the full list of companies here.

The results contrast starkly with the MSLP’s paltry aid to clean energy companies, which received just nine loans totaling $62 million, for an average size of $6.9 million. Excluding the two bigger loans of $25 million and $22.6 million, clean energy’s seven remaining loans averaged just $2.1 million.

As a portion of the loan portfolio, clean energy comprises 1% after drifting downward most months. Fossil fuels have captured more than 13% of the money, a figure that has increased in every month but one. That disparity raises questions about the Fed’s commitment to fighting the financial risks posed by climate change, which it only began to acknowledge publicly after this year’s election.

The troubled Main Street program is set to expire on Dec. 31, after a slow start and bureaucratic problems put a damper on its size and economic impact. Treasury Secretary Steven Mnuchin decided unilaterally last month, shortly after the election outcome was clear, that the programs would end in spite of worsening pandemic and weak economic signals. The move drew criticism from Fed Chair Jerome Powell and analysts across the political spectrum, who say pulling the plug prematurely will deprive the economy of crucial support as headwinds gather into the new year.

Critics of the decision to stop lending note that the incoming administration of President-elect Joe Biden can, and likely will, reopen the programs using a separate funding stream. If that happens, policymakers will have an opportunity to rewrite terms for the MSLP and other programs to support a sustainable recovery by excluding companies, including fossil fuels, with harmful environmental or social impacts.

Calling Mnuchin’s move to end the programs “a political decision,” Congressional Oversight Commission member Bharat Ramamurti said at a hearing Thursday that the new administration “can, and in my view should, restart the programs, reclaim the money Congress has set aside in the CARES Act, and use it to offer more help to small businesses and state and local governments.”

The MSLP aimed to help bridge the economic downturn for mid-sized businesses that were healthy before the pandemic. The loans are originated by banks, but the Fed buys them — and assumes the risk they will fail — if banks adhere to strict guidelines regarding borrowers’ finances.

Fossil fuel interests successfully pushed to modify the Fed’s original program design, which would have excluded many oil and gas companies already struggling with heavy debt burdens and repayment deadlines. In letters to the Fed, the Independent Petroleum Producers Association and Texas Senator Ted Cruz acknowledged that many drillers were on the brink of failure for reasons unrelated to COVID, but argued the companies still should be cushioned from record-low oil prices.

The Fed yielded on April 30, opening the program to more heavily indebted companies and those that would use the new loans to repay old ones. Energy Secretary Dan Brouillettte later said he had worked with Treasury and the Fed to increase drillers’ access to the program.

Loans purchased by the Fed through the MSLP rose to $6.3 billion in November from $4.2 billion the month before. With the program set to expire this month, banks have stopped accepting applications from borrowers, citing the limited time left to process them and result them to the Fed.

The Trump administration’s fossil fuel-friendly approach to emergency lending is at odds with a recent policy statement by world leaders, responding to a December 2nd UN report finding that major fossil fuel producers are set to expand production by 2%, while achieving Paris agreement goals would require a reduction of 6% per year. On Saturday, December 12, these leaders announced Six Climate-Positive actions to help rebuild economies from COVID-19 including “no bailout for polluting industries.”